The post has been translated automatically. Original language: Russian

In the first part of the material, they told how in six months they managed to launch a full-fledged digital bank for SMEs with fast transactions, foreign economic activity and a merchant's personal account. In the second part, we reveal the technological behind-the-scenes of the project: the best user scenarios on the market, an experimental design concept, a trending Flutter technical stack and progressive microservice architecture.

The bank was designed based on qualitative and quantitative research and taking into account the benchmarks of the CIS and the world. This is a conceptually different approach: we studied all market scenarios, tested each one and defended the best solution for each bank. Based on these target scenarios, the bank built and rebuilt the processes inside.

"Another challenge was that we had nothing to rely on: usually they either follow the path of as is to be, or copy the working functionality, transfer it to a new design and launch it. We designed from the ideal client path — and adjusted all processes for it both at us and at the bank," says Agiis Konkabayeva, CEO of red_mad_robot Central Asia.

According to the idea, the main page of the application should be organized as a stack of cards with information about the state of the business: account balances and transaction statuses, as well as operations that entrepreneurs most often turn to — statement and transfer to the counterparty. In the "My products" tab, now only the tariff, in the future all the bank's products will appear here. In the near future — online accounting and currency contracts.

"The content of the application now and in the future is based on the needs of the entrepreneur — the functionality that he faces and will face on a daily basis. The Bank is ready to connect both financial and non-financial services. And the backlog is thought out for a year ahead," she explained Agiis Konkabayeva, CEO of red_mad_robot Central Asia.

Therefore, the bank and its digital partner have set themselves the goal that in the first release, three main functions of the service will work fully at once.

1. Daily banking. Open an account, receive and send payments, see the current balance and transaction history — this is the base from which any bank starts for an entrepreneur. It is important to do this quickly and conveniently both in the digital channel and inside the bank: to give the entrepreneur the right speed for his operations — to simplify communication and speed up payments.

2. Foreign economic activity. It was not immediately decided to include foreign economic activity in the first release. But the market analysis showed that more and more entrepreneurs from different business segments of Kazakhstan are already engaged in foreign economic activity — for example, the trade turnover with the EAEU countries in January-April 2023 amounted to $9.5 million, which is 12% more than in 2022. Kazakhstan's trade with China is also growing: in the period from January to May 2023, its volume increased by 21.6%, to $10.7 billion. For the same period in 2022, the figure was $8.8 billion. At the same time, entrepreneurs often do not have accountants in the state and face certain difficulties.

"Usually, most of the tasks of foreign economic activity entrepreneurs are solved in Internet banking, banks bring minimal functionality to mobile applications. Our goal is to simplify foreign trade and make all the functionality available in a smartphone, based on previous experience of transferring foreign trade clients to a mobile application. At the same time, the focus was kept on the needs of not only large and medium-sized businesses, but also micro and small business entrepreneurs," commented Arina Lepikhova, Head of Digital SME Home Credit Bank.

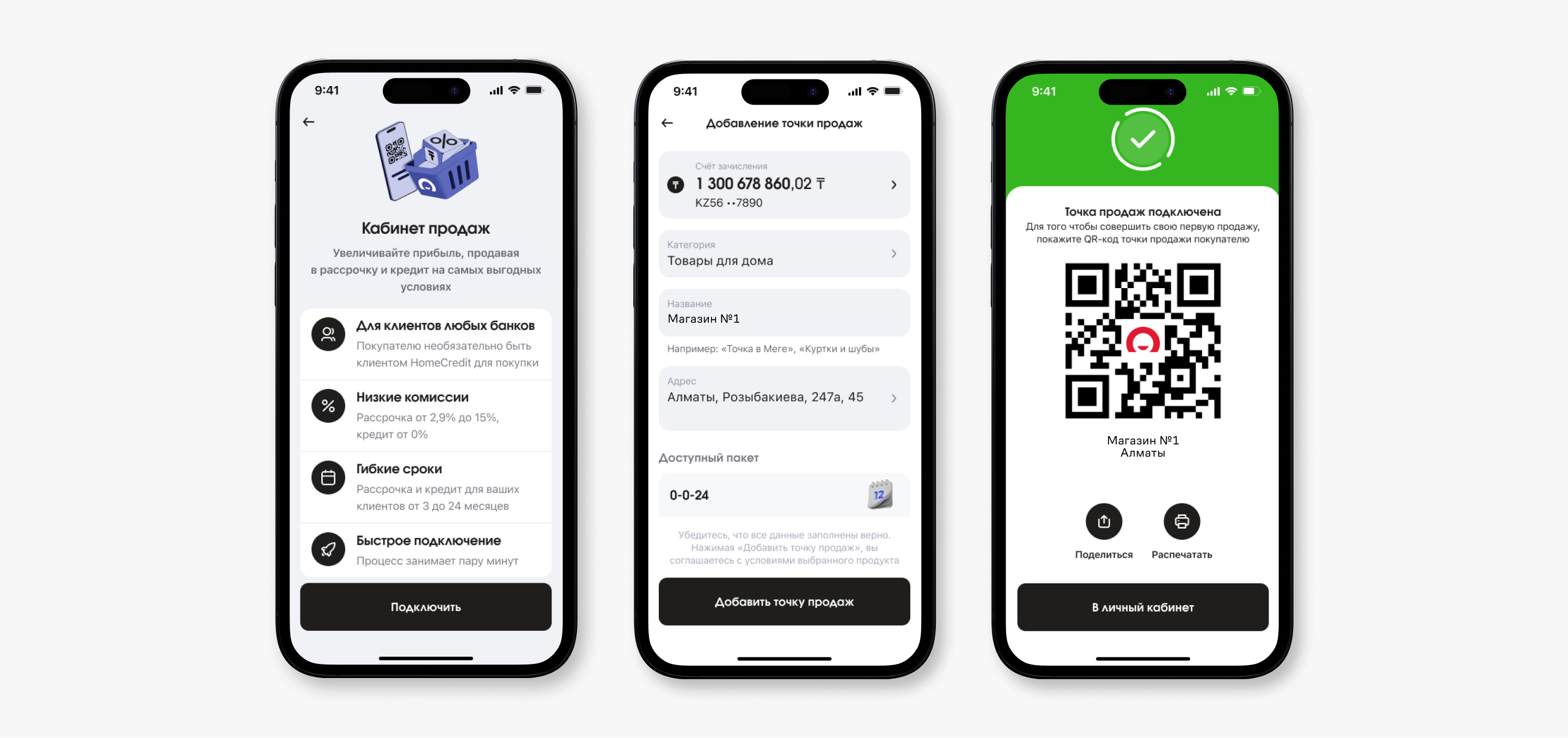

3. The personal sales account also appeared in the first release as a tool that helps to track statistics and increase business turnover using installment programs. Now it displays the number of sales per day and the balance. In the future, there will be a dashboard with summary information about the business: income and expenses for the period, the dynamics of sales in a slice, growth dynamics, forecasts of growth and decline, or a portfolio of assets.

The design concept, like other solutions, r_m_r CA was also defended before the bank, having collected an evidence base. The focus was to cover the needs of entrepreneurs, not to distract from the main tasks and to natively integrate the application into the daily life of the user. Therefore, we chose a minimalistic solution with two accent colors — black and red.

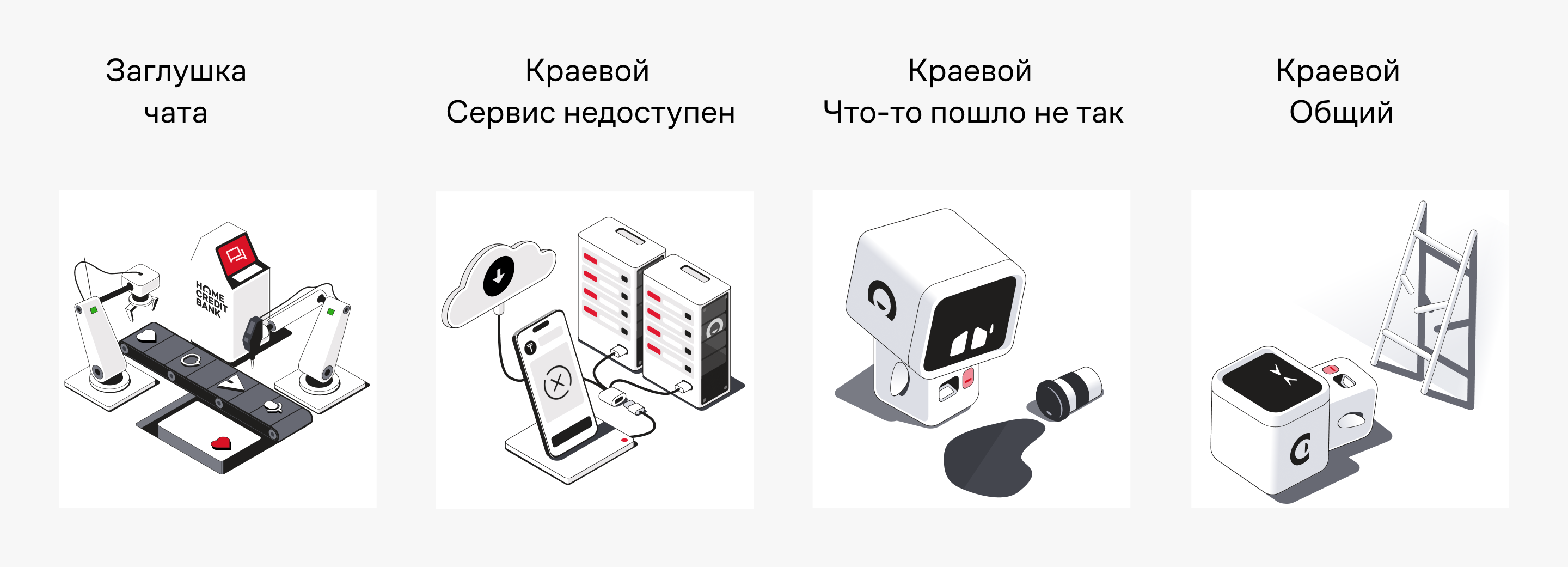

They abandoned the popular 3D illustrations that are used everywhere, in favor of the style that the team called "dvaton-isometry" - 2D illustrations that simulate 3D. There has not been such a solution on the market yet.

In the screens with errors, we took the path of leveling the negative in order to dilute the possible unpleasant impression of the user with an illustration. So there was a cute robot that gets into various embarrassing situations.

The Flutter framework, an innovative cross—platform development technology from Google, was chosen as the technical stack.

Home Credit Bank uses Flutter in the development of other products, so it would be easier to integrate the new solution into the bank's systems.

"The development phase began with a study of the bank's IT landscape. We have identified the key technologies that can be used in the implementation. We agreed on transparent rules for the introduction of new IT components and libraries for the bank, which had to be approved by the architectural committee and coordinated with information security," says Alexander Kuttukov, CTO red_mad_robot Central Asia.

Flutter allows you to develop one application for two mobile platforms iOS and Android at once, so we managed to significantly gain in speed, which was important for each of the stages of the project. It was not without difficulties. There are few banking applications developed on Flutter in the world practice, although this is an upward trend: Alibaba, Ebay, Google Ads and others work with it. We needed the best platform specialists, which are almost non-existent in the country. But in red_mad_robot, this practice is actively developing, so we managed to attract the best developers.

Choosing the architecture of the application, we kept in focus the ambitious goal of Home Credit Bank to enter the top 3 digital banks for entrepreneurs in Kazakhstan - for this, the bank must be convenient, accessible 24/7 and, most importantly, easily scaled in services.

Therefore, a microservice architecture was chosen. Unlike Monolith, it gives flexibility and speed, allowing you to develop functionality by independent teams and reduce time-to-market. And an application with a microservice architecture allows you to flexibly scale services, thanks to which it is able to withstand a growing flow of users and provide a high response rate. It was important to lay the right foundation to enable the bank to go in this direction and help spread the best practices inside.

We managed to meet the tight deadlines at this stage, among other things, thanks to the synchronization of red_mad_robot Central Asia and the bank's IT team, with which there was an open and effective interaction.

It was possible to achieve a full-fledged result in an unprecedented six months thanks to partnership interaction with the client, effective project management and technological expertise of red_mad_robot Central Asia.

"We have so penetrated into the client's processes that sometimes the Home Credit Bank team can work in the red_mad_robot office – and vice versa. This is what we call insourcing — like outsourcing, only better. Because the team that works for you combines the best qualities of outsourcing: the expertise of the external market, the economic advantages of an external contractor, business expertise and the main advantages of inhouse - immersion in the problems and tasks of the customer, as in their own," she shared Agiis Konkabayeva, CEO of red_mad_robot Central Asia.

At the start, it was decided that the entire development would be incremental and concrete results should be given every two weeks. Therefore, we immediately decided to follow the Scrum framework.

We worked in sprints with transparent goals, previously jointly agreeing on them. This allowed us to see and record real progress. As part of the sprints, secondary studies and demos were conducted on the bank's team, and functionality was also tested.

We divided the teams into four streams based on the functionality they were developing:

- core banking

- payments

- Foreign economic activity

- personal sales account.

This facilitated communication and unloaded regular meetings. Each stream had a project manager, designer, developer and analyst who were responsible for a specific scenario.

We have agreed with the Home Credit Bank team on areas of responsibility, work processes, decision-making points and escalation, and in each stream we have established basic hygiene for the production cycle.

It was important to see transparently at what stage the work of the streams is throughout the project. This made it possible to effectively manage changes in live mode.

"For some time, I took over the synchronization and implementation within the bank's systems — I built processes, backlog management, project management, participated with IT in the formation of areas of responsibility and initiated the allocation of resources to core teams across the bank's departments. A little later, product owners and business analysts joined my team - this helped, together with r_m_r CA, to create new business processes and quickly master them," comments Arina Lepikhova, Head of Digital SME Home Credit Bank.

At the start, the team consisted of 10 people, now more than 70 are working on the project: developers, designers, managers, analysts are one of the largest project teams in red_mad_robot Central Asia.

In six months, the way was passed from the beginning of the design from scratch to the publication of the application in stores. This is an unprecedented period for the world and Kazakhstan markets.

What have you done:

- We launched a digital bank for entrepreneurs from scratch in record time.

- We implemented the functionality of basic daily banking and made a personal sales account for sellers.

- Launched the function of online management of foreign economic activity.

"We managed to do all this thanks to digital partnership, well-coordinated joint work with the bank, business expertise and technological competencies of the team. The experience of working with Home Credit Bank once again confirms that red_mad_robot Central Asia's ambition to become a top-1 IT company in the Kazakhstan market is fully justified. We have all the unique competencies to make large-scale digital products in the Central Asian market in a short time and change this market, showing concrete results," emphasizes Agiis Konkabayeva, CEO of red_mad_robot Central Asia.

The Central Asian market is already showing a tendency to quickly create products and accelerate time-to-market: competition is growing, there are fewer free niches and delay leads to lost profits. It is important to quickly assess the market situation, design and launch the best solutions and flexibly respond to growing user requests, relying on the expertise of strong digital partners.

В первой части материала рассказали, как за полгода удалось запустить полноценный цифровой банк для МСБ с быстрыми транзакциями, ВЭД и личным кабинетом мерчанта. Во второй части приоткрываем технологическое закулисье проекта: лучшие на рынке пользовательские сценарии, экспериментальная дизайн-концепция, трендовый технический стек Flutter и прогрессивная микросервисная архитектура.

Банк проектировали, отталкиваясь от качественного и количественного исследования и учитывая бенчмарки СНГ и мира. Это концептуально иной подход: изучили все рыночные сценарии, протестировали каждый и для каждого защитили банку лучшее решение. Исходя из этих целевых сценариев банк выстраивал и перестраивал процессы внутри.

«Ещё один вызов состоял в том, что нам не на что было опираться: обычно либо идут по пути as is to be, либо копируют работающую функциональность, переносят в новый дизайн и запускают. Мы же проектировали от идеального клиентского пути — и под него подстраивали все процессы как у нас, так и в банке», - рассказывает CEO red_mad_robot Central Asia Агиис Конкабаева.

По задумке, главная страница приложения должна быть организована как стек карточек с информацией о состоянии бизнеса: остатки на счетах и статусы операций, а ещё операции, к которым предприниматели обращаются чаще всего — выписка и перевод контрагенту. Во вкладке «Мои продукты» сейчас только тариф, в дальнейшем здесь будут появляться все продукты банка. В ближайшей перспективе — онлайн-бухгалтерия и валютные контракты.

«Наполнение приложения сейчас и в перспективе основано на потребностях предпринимателя — функциональности, с которой он сталкивается и будет сталкиваться ежедневно. Банк готов к подключению и финансовых, и нефинансовых услуг. А бэклог продуман на год вперёд», - пояснила Агиис Конкабаева, CEO red_mad_robot Central Asia.

Поэтому банк и его цифровой партнёр поставили себе цель, что в первом релизе будут полноценно работать сразу три главные функции сервиса.

1. Дейли банкинг. Открыть счёт, получать и отправлять платежи, видеть текущий баланс и историю операций — это база, с которой начинается любой банк для предпринимателя. Важно делать это быстро и удобно как в цифровом канале, так и внутри банка: дать предпринимателю нужную скорость для его операций — упростить коммуникацию и ускорить платежи.

2. ВЭД. Включать ВЭД в первый релиз решили не сразу. Но анализ рынка показал, что всё больше предпринимателей разных сегментов бизнеса Казахстана уже занимаются внешнеэкономической деятельностью — так, товарооборот со странами ЕАЭС в январе-апреле 2023 года составил $9,5 млн, что на 12% больше показателей 2022 года. Растёт и торговля Казахстана с Китаем: в период с января по май 2023 года её объем вырос на 21,6%, до $10,7 млрд. За тот же период 2022 года показатель составил $8,8 млрд. При этом зачастую предприниматели не имеют бухгалтеров в штате и сталкиваются с определёнными сложностями.

«Обычно большинство задач предпринимателей ВЭД решаются в интернет-банке, в мобильные приложения банки выносят минимальную функциональность. Наша цель — упростить ВЭД и сделать доступным всю функциональность в смартфоне, опираясь на предыдущий опыт перевода ВЭД-клиентов в мобильное приложение. Фокус при этом держали на потребностях не только крупного и среднего бизнеса, но и предпринимателей микро- и малого бизнеса», - прокомментировала Арина Лепихова, Head of Digital SME Home Credit Bank.

3. Личный кабинет продаж тоже оказался в первом релизе как инструмент, который помогает отслеживать статистику и увеличивать обороты бизнеса с помощью программ рассрочки. Сейчас он отображает количество продаж за день и баланс. В перспективе там появится дашборд со сводной информацией относительно бизнеса: доходы и расходы за период, динамика продаж в срезе, динамика роста, прогнозы о росте и падении или портфель активов.

Дизайн-концепцию, как и другие решения, r_m_r CA тоже защищали перед банком, собрав доказательную базу. В фокусе было закрывать потребности предпринимателей, не отвлекать от главных задач и нативно встроить приложение в повседневность пользователя. Поэтому выбрали минималистичное решение с двумя акцентными цветами — чёрным и красным.

Отказались от популярных 3D-иллюстраций, которые используют повсеместно, в пользу стиля, получившего в команде название «дватон-изометрия», – 2D-иллюстраций, которые имитируют 3D. Такого решения на рынке ещё не было.

В экранах с ошибками пошли по пути нивелирования негатива, чтобы разбавить иллюстрацией возможное неприятное впечатление пользователя. Так появился милый робот, который попадает в разные конфузные ситуации.

В качестве технического стека выбрали фреймворк Flutter — инновационную технологию кроссплатформенной разработки от Google.

Home Credit Bank использует Flutter в разработке других продуктов, поэтому интегрировать новое решение в системы банка было бы проще.

«Этап разработки начали с исследования ИТ-ландшафта банка. Определили ключевые технологии, которые допустимо использовать при реализации. Договорились о прозрачных правилах внедрения новых для банка ИТ-компонентов и библиотек, которые необходимо было утвердить на архитектурном комитете и согласовать с информационной безопасностью», - рассказывает Александр Куттуков, CTO red_mad_robot Central Asia.

Flutter позволяет вести разработку одного приложения сразу под две мобильные платформы iOS и Android, поэтому удалось существенно выиграть в скорости, что было важно для каждого из этапов проекта. Не обошлось и без сложностей. В мировой практике мало банковских приложений, разработанных на Flutter, хотя это восходящий тренд: с ним работают Alibaba, Ebay, Google Ads и другие. Нужны были лучшие специалисты по платформе, которых в стране почти нет. Но в red_mad_robot эта практика активно развивается, поэтому удалось привлечь лучших разработчиков.

Выбирая архитектуру приложения, держали в фокусе амбициозную цель Home Credit Bank войти в топ-3 цифровых банков для предпринимателей Казахстана — для этого банк должен быть удобным, доступным 24/7 и, главное, легко масштабироваться в сервисах.

Поэтому была выбрана микросервисная архитектура. В отличие от монолита, она даёт гибкость и скорость, позволяя разрабатывать функциональность независимыми командами и сокращать time-to-market. А ещё приложение с микросервисной архитектурой позволяет гибко масштабировать сервисы, благодаря чему способно выдерживать растущий поток пользователей и обеспечивать высокую скорость отклика. Было важно заложить правильный фундамент, чтобы дать возможность банку идти в эту сторону и помочь распространить внутри лучшие практики.

Уложиться в сжатые сроки и на этом этапе удалось в том числе благодаря синхронизации red_mad_robot Central Asia и ИТ-команды банка, с которой сложилось открытое и эффективное взаимодействие.

Достичь полноценного результата за беспрецедентные шесть месяцев получилось благодаря партнёрскому взаимодействию с клиентом, эффективному проектному управлению и технологической экспертизе red_mad_robot Central Asia.

«Мы настолько проникли в процессы клиента, что иногда команда Home Credit Bank может работать в офисе red_mad_robot – и наоборот. Это то, что мы называем инсорсингом — как аутсорсинг, только лучше. Потому что команда, которая у тебя работает, объединяет в себе лучшие качества аутсорса: экспертизу внешнего рынка, экономические преимущества внешнего подрядчика, бизнес-экспертизу и главные преимущества инхауса — погруженность в проблемы и задачи заказчика, как в свои собственные», - поделилась Агиис Конкабаева, CEO red_mad_robot Central Asia.

На старте было решено, что вся разработка будет инкрементальная и каждые две недели нужно выдавать конкретные результаты. Поэтому сразу приняли решение идти по фреймворку Scrum.

Работали спринтами с прозрачными целями, предварительно совместно договариваясь о них. Это позволяло видеть и фиксировать реальный прогресс. В рамках спринтов проводили вторичные исследования и демо на команду банка, а ещё тестировали функциональность.

Разделили команды по четырём стримам, исходя из функциональности, которую они разрабатывали:

- core banking

- платежи

- ВЭД

- личный кабинет продаж.

Это облегчало коммуникацию и разгружало регулярные встречи. В каждом стриме был менеджер проекта, дизайнер, разработчик и аналитик, которые отвечали за конкретный сценарий.

Договорились с командой Home Credit Bank о зонах ответственности, рабочих процессах, точках принятия решений и эскалации, а в каждом стриме наладили базовую гигиену для производственного цикла.

Было важно прозрачно видеть, на каком этапе находится работа стримов на протяжении всего проекта. Это позволяло в живом режиме эффективно управлять изменениями.

«На некоторое время синхронизацию и внедрение внутри систем банка взяла на себя я — выстраивала процессы, управление бэклогом, проектное управление, участвовала с ИТ в формировании зон ответственности и инициировала выделение ресурсов на core-команды по департаментам банка. Чуть позже ко мне в команду вышли product owner-ы и бизнес-аналитики — это помогло вместе с r_m_r CA создать новые бизнеc-процессы и быстро их освоить», - комментирует Арина Лепихова, Head of Digital SME Home Credit Bank.

На старте команда состояла из 10 человек, сейчас над проектом работает уже больше 70: разработчики, дизайнеры, менеджеры, аналитики — одна из самых больших проектных команд в red_mad_robot Central Asia.

За шесть месяцев был пройден путь от начала проектирования с нуля до публикации приложения в сторах. Это беспрецедентный срок для мирового и казахстанского рынков.

Что сделали:

- Запустили с нуля цифровой банк для предпринимателей в рекордные сроки.

- Внедрили функциональность базового дейли банкинга и сделали для продавцов личный кабинет продаж.

- Запустили функцию онлайн-управления ВЭД.

«Всё это удалось сделать благодаря цифровому партнёрству, слаженной совместной работе с банком, бизнес-экспертизе и технологическим компетенциям команды. Опыт работы с Home Credit Bank в очередной раз подтверждает, что амбиция red_mad_robot Central Asia стать топ-1 ИТ-компанией на рынке Казахстана вполне оправдана. У нас есть все уникальные компетенции делать масштабные цифровые продукты на рынке Центральной Азии в короткие сроки и менять этот рынок, показывая конкретные результаты», - подчеркивает Агиис Конкабаева, CEO red_mad_robot Central Asia.

Рынок Центральной Азии уже сейчас показывает тенденцию на быстрое создание продуктов и ускорение time-to-market: конкуренция растёт, свободных ниш становится меньше и промедление ведёт к упущенной прибыли. Важно быстро оценивать рыночную ситуацию, проектировать и запускать лучшие решения и гибко откликаться на растущие запросы пользователей, опираясь на экспертизу сильных цифровых партнёров.

Share

Share